Fico Score vs Credit Score: How They Work, the Difference & Why It Matters

- Credit Repair Ease

- Jan 9, 2023

- 7 min read

Both a Fico score and a credit score are used to measure your creditworthiness, but they use different formulas and weigh different factors. so, before the reach out conclusion understand between Fico Score vs Credit Score. Your Fico score is based on information from your credit report, while your credit score is based on the risk factors of all consumers. Knowing the difference between these two scores can help you understand why your credit might be lower than you expected or what you need to do to improve it.

If you've ever applied for a loan, you've probably had to provide your FICO score. But what is a FICO score, and how is it different from a credit score? what is the difference between Fico Score vs Credit Score? In this post, we'll break down the differences between these two scores and explain why they both matter. By understanding the difference between FICO and credit scores, you can make sure you're getting the best rate on your next loan.

What is a Fico Score and how does it work?

A Fico score is a three-digit number that is meant to represent your creditworthiness. It is created by the Fair Isaac Corporation and is used by lenders when you are applying for a loan or a credit card. The score takes into account various factors, including your payment history, the amount of debt you have, and how long you've had credit. Your Fico score can range from 300 to 850, and the higher it is, the better your chances of getting approved for a loan or credit card. Knowing what goes into your Fico score and taking steps to improve it can help you get approved for products with better terms and save money on interest payments.

How is your Fico Score calculated?

Fico Score is a credit score that is used by lenders to assess the creditworthiness of a borrower.

A Fico Score is calculated by looking at your credit history and then assigning you a number between 300 and 850, with 850 being the best.

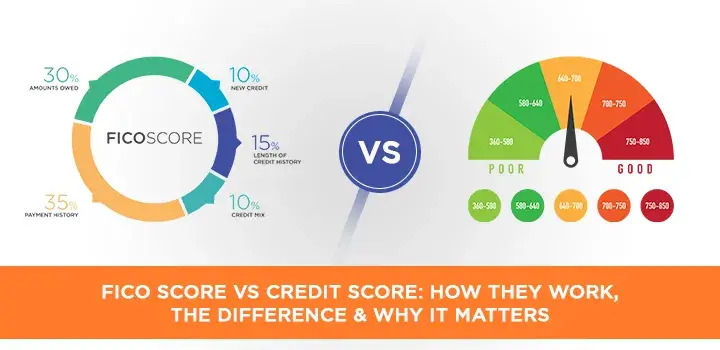

FICO Scores are based on five factors:

1. Payment History (35%)

2. Amounts Owed (30%)

3. Length of Credit History (15%)

4. New Credit (10%)

5. Types of Credit Used (10%).

Why is your Fico Score important?

When you're applying for a loan, your credit score is one of the most important factors that the lender will consider. Your Fico score ranges from 300 to 850, and it measures how likely you are to repay your debt. A high Fico score can help you get a lower interest rate on a loan, while a low Fico score could mean that you won't be approved for a loan at all. So, what can you do to make sure your Fico score is as high as possible?

How can you improve your Fico Score?

Your Fico Score is important. It's one of the factors that lenders look at when considering you for a loan or credit card. So, it's important to make sure your score is as high as possible. Here are some tips on how to improve your Fico Score.

1. Check your credit report for mistakes and correct them

2. Pay your bills on time

3. Keep your credit utilization low - don't max out your credit cards

4. Don't apply for too many new credit cards at once

5. Don't close old accounts, especially if they have a long history of good payment behavior

6. Don't make too many big purchases in a short period of time

What are some of the factors that affect your Fico Score?

1. Payment history - whether you've paid your bills on time

2. Amounts owed - how much credit you have compared to the amount of debt you owe

3. Length of credit history - how long you've had credit accounts open

4. New credit - applying for new lines of credit can lower your score

5. Types of credit used - a mix of installment loans, revolving lines of credit, and mortgage loans are ideal

6. Credit utilization rate - using a high percentage of your available credit can hurt your score

What is a Credit Score and how does it work?

What is a credit score? A credit score is a number that reflects your credit history and shows lenders how likely you are to repay your debts. Your credit score can range from 300-850, and the higher your score, the better interest rate you'll likely receive on a loan or mortgage. Your credit score is calculated based on five factors: payment history, amount of debt, length of credit history, new credit inquiries, and type of credit used.

How is your credit score calculated and how to improve your credit score?

Many people don't know how credit scores are calculated but understanding the process can be helpful in managing your credit and improving your score. There are a few different credit scoring models in use today, but the most common is the FICO score. This score is based on five factors:

1. Payment History (35%)

2. Credit Utilization (30%)

3. Credit History (15%)

4. Credit Mix (10%)

5. New Credit (10%)

As you can see, payment history is the most important factor in your credit score. That's why it's so important to make all your payments on time and to keep your credit card balances low. By following these simple steps, you can help improve your credit score and get on the path to financial success.

The benefits of having a good credit score

A credit score is a number that lenders use to evaluate a potential borrower’s creditworthiness. a credit score is calculated using information from credit reports, which are maintained by credit bureaus. credit scores range from 300 to 850, and the higher the score, the better. A good credit score can save borrowers Thousands of dollars in interest over the life of a loan. For example, a borrower with a credit score of 780 can expect to pay about $300 less in interest on a $20,000 loan than a borrower with a credit score of 680. In addition to lower interest rates, good credit can also lead to faster approval for loans and credit cards, and even better terms on insurance policies. Simply put, a good credit score is essential for anyone who wants to access affordable borrowing.

What happens if you don't have a good credit score?

A bad credit score could lead to a higher interest rate and less favorable loan terms. In some cases, you may not be approved for a loan at all. Your credit score is calculated using information from your credit report, including your payment history, credit utilization, and credit mix. The higher your credit score, the lower the risk you pose to lenders. If you have a low credit score, you may want to consider ways to improve it before applying for a loan. There are many resources available to help you understand and improve your credit score.

Why your credit score matters for more than just getting a loan or mortgage

Most people are aware that their credit score is important for things like taking out a loan or getting a mortgage. However, credit scores can also have an impact on other areas of your life. For example, your credit score is often used as a factor in determining insurance rates. And if you're looking to rent an apartment, most landlords will check your credit score as part of the screening process. So even if you're not planning on applying for credit anytime soon, it's still important to maintain a good credit score. But how is your credit score calculated? The answer is quite simple: credit scores are based on the information in your credit report. This includes things like your payment history, outstanding debt, and credit utilization ratio. By maintaining a healthy credit report, you can help ensure that you have a good credit score - which can save you money and stress down the road.

Tips for maintaining a good credit score over time

If you have a low credit score, it means that you have not managed your credit well in the past. There are several things you can do to improve your credit score. You can get a copy of your credit report from the three credit bureaus and check for errors. You can also start paying your bills on time, keep your credit balances low, and avoid opening new credit lines if you don't need them. By taking these steps, you can improve your credit score over time.

FICO score vs. Vantage Score

There are two main credit scoring models used by lenders in the United States: the FICO score and the Vantage Score. Both models use similar information to calculate a score, but there are some important differences to be aware of.

The FICO score was introduced in 1989 and is still the most widely used credit score. It ranges from 300 to 850, with a higher score indicating better creditworthiness. The FICO score is based on five factors: payment history (35%), credit utilization (30%), length of credit history (15%), types of credit used (10%), and recent credit activity (10%).

The Vantage Score was introduced in 2006 and is gradually gaining acceptance among lenders. It ranges from 300 to 850, like the FICO score, but uses a different scoring system. The Vantage Score is based on six factors: payment history (40%), age and type of credit (21%), usage patterns (20%), balances (11%), Available Credit (5%) and recent inquiries (3%). Depending on the lender, you may have a higher or lower Vantage Score than the FICO score.

Both the FICO score and the Vantage Score are important when it comes to getting approved for loans and other forms of credit. Lenders will typically look at both scores when making a decision, so it's important to understand both models. If you have any questions about your score, be sure to ask your lender for more information.

Conclusion:

A FICO score and credit score are important factors that lenders look at when considering a loan or line of credit. It's essential to understand the difference between the two and how they work. Strong credit history can save you money in interest payments and give you more negotiating power when it comes time to apply for a loan.

If you have any questions about your FICO score vs credit score, don't hesitate to give us a call at (888) 803-7889.

Comments